One of the most critical pieces about an operating model (or budget), is sales forecasting

One of the first frameworks on which the management team must align is the sales forecast. Final sales projections will ultimately be approved by the CEO, but the team must understand and agree on how they plan to forecast sales. The sales forecasting methodology should start by determining the underlying metrics or KPIs by which the company’s sales and marketing team measure growth. From there, it is important to layer in any business seasonality or planned metric improvements.

Here is an example:

Say the sales and marketing team measures performance by tracking sales unit velocity of individual products or services. A bottom-up approach might estimate the number of units of each SKU the team plans to sell each month for the next year and multiply the sales quantity by the average sales price.

There are many ways to look at this on an even more granular level, but this basic framework creates a measurable benchmark. If January was projected to sell 100 units, but the team sold 90, then it can be assumed that the variance of actual sales dollars to budgeted sales dollars can be explained. Ask management why the team only sold 90 units as opposed to 100. Maybe each customer ordered fewer units per order than expected, or perhaps there were fewer overall customers coming through the door. There can be multiple explanations; however, if teams can anticipate questions like this, they can proactively create their budget at this depth.

If management prioritizes a budget with this level of granularity and the company misses budget during the year, they will not only be able to explain why they missed budget with greater speed and clarity, but they will also be able to adapt and correct the underlying business processes moving forward.

I always recommend prioritizing the sales model first. The sales model usually takes the longest to generate and requires ongoing discussions and tweaks as the cost side of the operating model is built out. Say your team develops an independent sales forecast of $1,000,000 for next year. Then in November, department leaders submit their vendor-level budgets for approval. When all department budgets are combined, they total up to $1,500,000. If the corporate objective is to be profitable next year, the management team cannot approve $1,500,000 in expenditures. Clearly, the team needs to either take a second look at the sales forecast or go back to department owners to reevaluate their budgeted expenditures.

Specifically, here are two requests you can ask of your team to accomplish a more streamlined sales forecasting process:

- In early October, ask your FP&A team to request a sales forecast directly from the sales and marketing team (due back in two weeks).

- Request the forecast be broken down by month, customer, product line, or any other KPI or level of detail that might be important to the CEO or sales leadership.

With these two tasks in mind, the sales and marketing team can then create their own goals and KPIs for the next year. This strategy also helps to prevent a deflection of ownership from the sales and marketing team. The sales forecast should be based on the underlying KPIs that the sales and marketing team are tracking on a weekly, monthly, or quarterly basis. If they are unable to provide an annual sales forecast or have never built one before, walk them through it. Use this as a collaborative experience for both departments to develop a new methodology together.

Keep in mind, it is important to be very clear with sales leadership to emphasize that they are ultimately responsible for the final sales budget published to the board. The FP&A team can analyze historical data and provide recommendations for a first draft, but it must be handed off to sales leadership to own and create their own model since they are responsible for the actual sales that will ultimately be measured.

Throughout the process, it is important to remember that budget processes must have buy-in from both the CEO and entire executive team, and they must facilitate this cooperation between different departments. Otherwise, the whole process breaks apart.

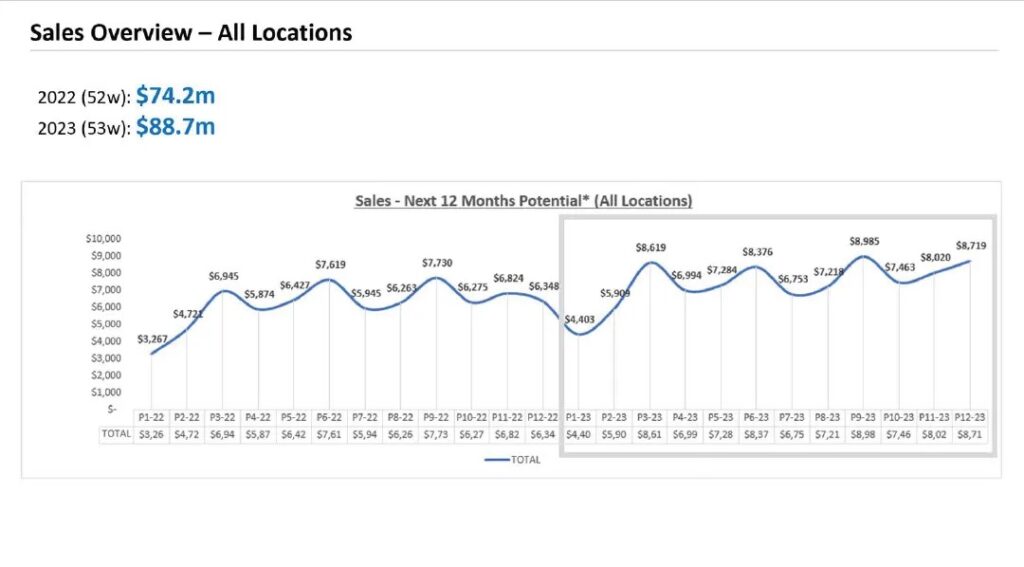

Case study: restaurant group

The sales forecasting framework in this hospitality and restaurant organization can be distilled into sales by week and by restaurant location.

There is no right or wrong answer in how to forecast or which KPIs to use in your methodology. The key to building a sales forecast is first to understand how the business behaves throughout the year, then develop a framework around that behavior.

In the restaurant space, I know that operators focus on weekly time periods. I also know each week of the year behaves differently for different restaurant locations. If the restaurant is located on a college campus, then sales plummet during summer and winter breaks. Holidays also result in lower sales than other times of year.

For this client, the two concepts I knew management tracked and felt were important to the business were:

- Weekly seasonality

- Individual restaurant location performance

When actual results are eventually published, having a sales forecast tool broken down by location and week gives the management team a benchmark to better understand the drivers of each location’s performance. If a location is underperforming, management could identify which factors might have been the specific culprit. Maybe scaffolding outside was scaring customers away. Maybe winter summer weather kept people home certain weeks so sales collapsed during those periods.

If the team had to forecast corporate sales using a top-down method, they might have put a blanket, weekly sales target in place that does not consider the core KPIs that I used in the example above. In other words, if management simply said, “All of our restaurants should hit $30,000 per week in sales combined” it would be difficult to identify the specific driver of any deviation in sales from that target since more granular, weekly seasonality or specific location performance was not considered.

Budgeting from the bottom up is not just about explaining variances. It is about arming management teams with tools that can help reveal problems or areas of success within their business.

General steps to get started with creating a bottom-up sales forecast:

- Determine the core sales metrics and KPIs that are important to your business. These metrics should be those that you can quantify to measure growth (Average Order Value (AOV), customer acquisition, sales unit velocity, etc.)

- Segment these sales metrics. This will allow you to achieve more granularity in your forecast (break it down by business line, product line, customer, geographical location, sales platform, or sales rep team).

- Identify historical seasonality (daily, weekly, or monthly). I.e., do your customers’ purchasing behaviors change over the course of the year?

- Forecast the year’s seasonality.

- Apply the seasonality to the sales metrics previously determined in step 1.

- Assign dollar values to the forecasted sales metrics or KPIs (If you choose to forecast quantities of sales units throughout the year, what is the average sales price per unit?).

- Run this exercise across all business segments, customers, product lines, etc.

- Sum all forecasted segments together to arrive at a corporate total.

Remember, work with management to determine if the total corporate sales budget makes sense. If not, try to isolate which component of the sales forecast does not make sense. Does your projected seasonality deviate from historical seasonality? Is your average sales price in line with recent product sales or a planned price hike? Does one business line’s projected sales performance seem out of line with historical trends or future growth initiatives? The more you run this exercise, the more proficient your team will become at budgeting and creating operating models.